In Washington energy policy circles, China is often viewed either as the dominant exporter of clean energy technologies or as the world’s largest emitter of greenhouse gases (GHGs). This binary framing obscures a significant evolution in China’s approach to carbon management and accounting, which is reshaping its energy system. These shifts carry wide-ranging implications for China’s trade agenda, competitiveness in frontier technologies such as AI, and role in global governance, especially as Chinese exporters face growing external regulatory pressures. This dynamic is well recognized in policy debates surrounding trade and energy policy in Beijing and Brussels—as it should be in Washington.

The European Union’s Carbon Border Adjustment Mechanism (CBAM) has emerged as a particularly influential factor shaping China’s evolving approach to carbon governance. First proposed in 2019 as a part of the expansive European Green Deal and adopted as part of the “Fit for 55” package in March 2023 by the European Council, CBAM levies tariffs on carbon-intensive imported products to protect European producers that face carbon costs in the EU Emission Trading System (ETS). As this tariff can only be avoided by proving that an equivalent carbon price has been paid elsewhere, CBAM creates an incentive for other jurisdictions to develop credible carbon pricing and governance systems compatible with strict EU standards. This incentive has not gone unnoticed in China, which operates its own ETS partially modeled on the European system.

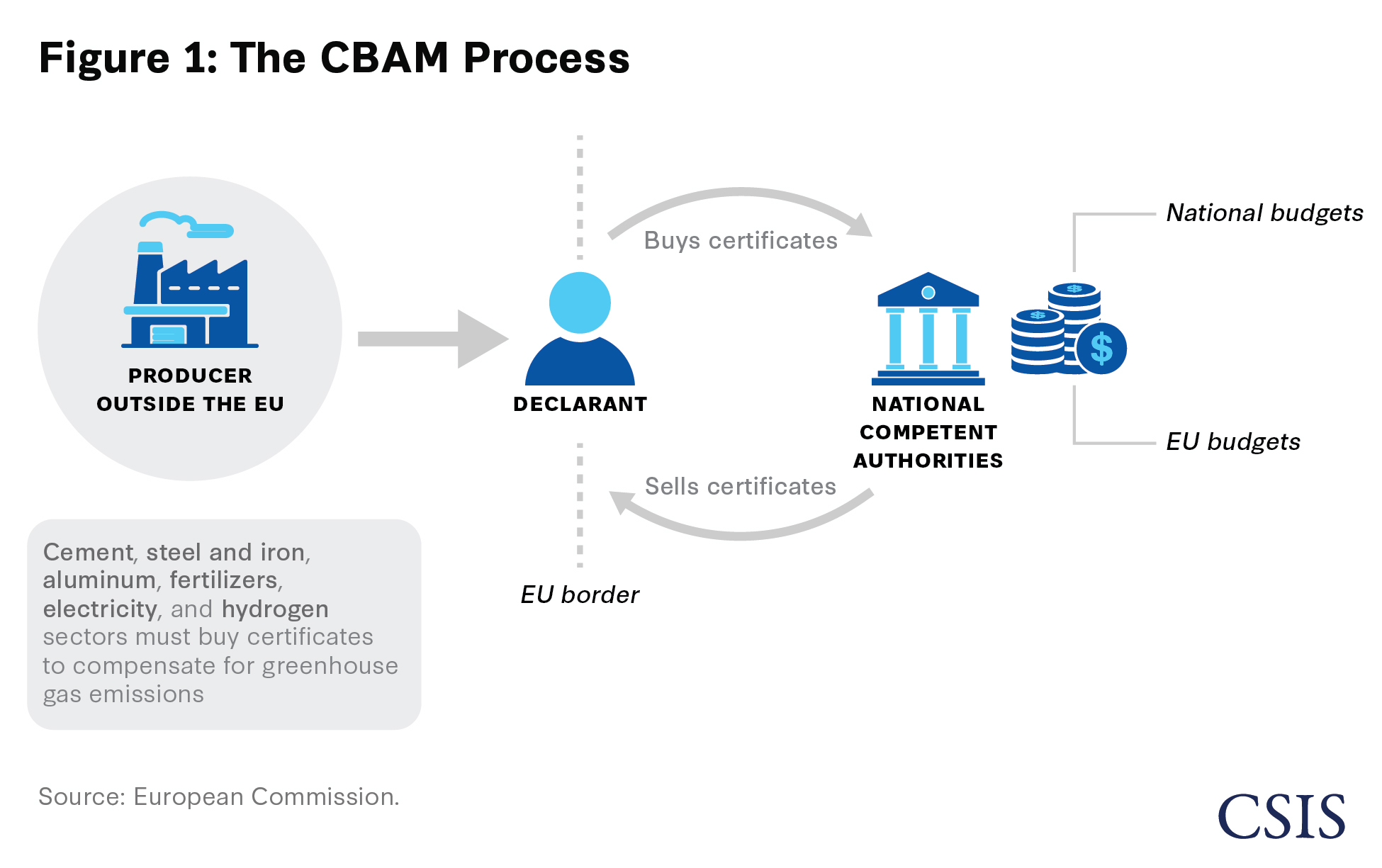

CBAM Explained

The first instrument of its kind to exist at the international level, CBAM is designed to prevent “carbon leakage,” or instances of EU emissions reductions being offset by production shifting to non-EU countries with higher embedded GHG emissions. CBAM requires exporters to pay for the costs of their emissions when entering the European market if they have not already done so in the country of production. Under current terms, EU importers must report the GHG emissions embedded in goods from the six covered categories—cement, fertilizers, electricity, iron and steel, aluminum, and hydrogen—on an annual basis and surrender a corresponding number of CBAM certificates. For the first quarter of 2026, CBAM certificates were priced at €75.36 per ton of CO2 emitted. Starting in 2027, certificate prices will be calculated using the weekly average auction price of EU ETS allowances. CBAM’s scope is expected to expand in 2028, with effects likely to be particularly pronounced for large exporters and carbon-intensive emerging economies such as China and India.

While a formal linkage between the Chinese and EU ETS remains unlikely in the foreseeable future, China’s approach to carbon governance may nevertheless become more institutionally aligned with Europe’s over the long term. Such convergence reflects the economic reality of deep bilateral trade ties and is already evident in the expected expansion of the Chinese ETS, stronger enforcement of carbon emission reporting and standard-setting, as well as local-level initiatives designed to support sectoral targets and help companies navigate carbon governance at home and abroad. Moving forward, the credibility of China’s compliance, monitoring, and enforcement will be central to both the success of its carbon governance efforts as well as international confidence in its approach.

Understanding whether and how China—the world’s largest emitter and many countries’ top trading partner—responds to CBAM has significant implications for both strategic and decarbonization objectives. For U.S. policymakers, the evolution of carbon governance in Europe and China matters not only for U.S. companies operating in or exporting to these major markets, but also for global governance: Deeper EU-China institutional alignment could complicate future transatlantic coordination or leave the United States out of a large carbon-adjusted trading bloc. If China succeeds in developing credible carbon governance in response to CBAM, it could inform the design and implementation of similar policies in other countries—even the United States. More broadly, China’s response may reveal how carbon tariffs and external regulation can nudge domestic reforms in major emitting economies.

What CBAM Means for China

Estimated Impacts

Studies issued by the EU Commission project that annual CBAM-related revenue could reach an average of about $1.5 billion from 2028. In 2024, 21.3 percent of goods imported into the European Union originated in China. This makes China the single largest exporter to the bloc, dwarfing the 13.8 percent from the United States, its second-largest trade partner. The proportion of Chinese exports to the European Union covered by CBAM is also the second highest of all trade partners, trailing only Russia.

In terms of emissions, Chinese exports to Europe generated an estimated 375 million tons of carbon emissions in 2021. In its current form, however, CBAM’s impact on China is relatively small: Goods from the six covered categories made up only 0.8 percent of China’s total EU exports in 2025, according to customs data. Iron and steel accounted for 92 percent of affected exports, followed by aluminum at 7 percent. One 2025 study found that CBAM could incur $1.4 billion in cost to China, which only represented about 0.3 percent of its total value of exports to the European Union that year.

Dual Carbon Goals

In a 2020 address to the UN General Assembly, President Xi Jinping pledged that China would reach peak CO2 emissions before 2030 and economy-wide carbon neutrality before 2060. Later that year, Xi announced complementary 2030 benchmark goals as part of China’s commitments under the Paris Agreement—including reducing carbon intensity by more than 65 percent from 2005 levels, raising the share of non-fossil energy to roughly 25 percent, expanding forest carbon sinks, and rapidly scaling wind and solar deployment. The “30/60” (or “Dual Carbon”) targets have played an important role in China. They are enshrined in key government strategy documents, including the 15th Five-Year Plan. In 2025, China committed to reducing GHG emissions by 7–10 percent from peak levels by 2035. While many observers have criticized the goal as too lax relative to China’s capabilities, it is the first time the country has aimed to reduce absolute emissions.

These projections, however, may understate CBAM’s longer-term impact. Starting in 2028, CBAM is expected to expand to about 180 steel- and aluminum-intensive products, including machinery components and household appliances. As coverage broadens along the value chain, particularly on downstream goods with high embedded emissions from primary inputs such as steel and aluminum, the magnitude of CBAM’s trade effects—and its burden on Chinese exporters—will definitely increase.

In China, the European Union’s plans for CBAM expansion are being taken as a serious economic issue. As early as 2021, the State Council’s Development Research Center published a report estimating that in an extreme scenario—where CBAM was extended to cover all Chinese exports—China’s GDP could fall by up to 0.64 percent, putting 2.3 million manufacturing jobs at risk and leading exports to the European Union to decline by around 13 percent by 2030. The study also warned that labor-intensive sectors and electronics manufacturers could be particularly exposed due to the higher carbon intensity of Chinese production. However, it is worth noting that such a drastic expansion of CBAM is unlikely and that Chinese exports to Europe have in fact increased in recent years despite the introduction of certain sectoral tariffs.

The Status of China’s Energy System and Carbon Governance

China’s exposure to CBAM is ultimately a function of the carbon intensity of its industrial production, which is in turn largely dependent on the structure of China’s energy system and its carbon pricing mechanism. Both sides of the equation have made advances in recent years, but still fall significantly short of European regulatory standards.

Energy Mix and Emissions

Although CBAM assesses the carbon intensity and pricing of specific exported goods rather than national emissions totals, the overall energy mix still matters for product-level footprints. For China, this picture is complicated (see Figure 2). Record growth in renewables and nuclear energy deployment—combined with moderating demand from heavy industry—has led some recent analyses to suggest that China’s CO2 emissions may already have peaked. Yet, China’s industrial production and broader economy remain comparatively energy- and emissions-intensive. In 2024, China emitted 0.39 kilograms of CO2e (carbon dioxide equivalent) per U.S. dollar of GDP on a purchasing power parity basis—roughly four times the EU average and twice the global average.

The role of coal in China’s energy mix and political economy remains at the heart of this challenge. As of 2024, coal accounted for 53 percent of China’s total energy consumption and 58 percent of its power generation, while non-fossil sources supplied roughly one-fifth of primary energy and one-third of electricity. For industrial sectors, coal supplied close to 34 percent of energy inputs in 2023, far above the European Union’s 9 percent and the global average of 23 percent. Further complicating the transition away from coal is a continued rise in China’s total energy use, which has quadrupled between 2000 and 2023 (see Figure 3). Though not yet a major source of electricity demand growth, data centers could also emerge as a new pressure point alongside China’s manufacturing-focused Covid recovery strategy, which has likely already contributed to the country missing its 2025 carbon intensity targets under the Paris Agreement.

Power Sector Reform

Aside from resource endowments and investment trends, China’s energy mix is also shaped by how electricity is dispatched and priced. Today, the country’s power system is governed by a hybrid system of both legacy administrative planning and expanding market-based mechanisms. Provincial dispatch centers and grid companies continue to play a central role in allocating generation, managing interprovincial flows, and maintaining system reliability, but a growing share of electricity is procured through long-term contracts, spot markets, or market-based retail arrangements for industrial and commercial users alike. Coal still underpins much of the system’s flexibility and reliability, but reforms to dispatch, pricing, capacity compensation, and renewable integration are increasingly intended to allow low-carbon resources to compete more effectively and be used when available. The extent to which renewables displace coal therefore depends as much on market prices, grid operations, and provincial incentives that support efficient dispatch and cross-regional electricity trading as on installed capacity.

ETS Governance

China’s ability to manage CBAM exposure will also depend on the credibility and functionality of its emissions governance. Today, China’s national ETS encompasses the power sector as well as steel, cement, and aluminum—carbon-intensive industries covered by CBAM—spanning roughly 3,000 firms and about 60 percent of national emissions. For now, the system remains relatively light-touch: Allowances are still largely free while compliance is based on carbon-intensity targets rather than absolute emissions caps. Although firms are unlikely to face a strong near-term carbon price burden, they will increasingly need to strengthen monitoring, reporting, and verification systems to disclose high-frequency, plant-specific data, rather than relying on annual averages.

China’s ETS is expected to expand to cover additional high-emission sectors, including chemicals, petrochemicals, paper, aviation, flat glass, and copper smelting, alongside a planned shift toward absolute caps and paid permits by 2030. Combined with a broader push for structured environmental, social, and governance reporting among listed Chinese firms, these changes could strengthen China’s carbon price signal and bring its market closer to the EU ETS. Even so, few experts expect ETS to be the main driver of emissions reductions in China, where command-and-control measures remain prevalent. Rather, its importance lies in helping close institutional gaps with the European Union while supporting longer-term reductions in carbon intensity and overall emissions.

China’s Emerging Carbon Governance

Rhetorical Resistance and Pragmatic Response to CBAM

Since CBAM’s inception, Chinese leaders have framed it as protectionist and harmful to global growth. In the country’s first statement on the policy in 2019, Vice Environment Minister Zhao Yingmin called it “unilateralist and protectionist,” with the potential to “hurt global growth.” In 2021, President Xi Jinping warned that climate action should not be “an excuse” for trade barriers, a message echoed by Premier Li Keqiang. China is also aligned with countries such as India that have been vocal in their criticism of CBAM in venues including the UN Framework Convention on Climate Change’s Conference of the Parties (COP). As recently as January 2026, Chinese Ministry of Commerce spokespersons were openly criticizing CBAM as a protectionist measure.

Despite repeated invoking of World Trade Organization (WTO) rules and public expressions of concern in WTO meetings, China has not brought a formal case against CBAM to the organization, as Russia elected to. CBAM is part of a broader set of trade-related issues that have affected relations between Brussels and Beijing, including high-profile tariffs on electric vehicle exports.

In practice, China’s policy responses have been considerably more pragmatic than its rhetoric suggests. In meetings with Chinese experts between 2024 and 2026, the authors learned that the central government has effectively allowed local authorities and companies to explore how to best ensure compliance with CBAM. Although CBAM is seen as a challenge, stakeholders recognize that the incentives provided by CBAM are aligned with long-term goals of the government enshrined in the 30/60 frameworks. The expansion of the Chinese ETS system, credited to CBAM by some experts interviewed by the authors, mirrors those goals. Publicly available official documents indicate that at least some parts of the Chinese government view the expansion of the Chinese ETS and engagement with standards as a key strategy to respond to CBAM.

Deep Dive: The Role of Local Governments

Since China announced its 30/60 goals—and especially since the European Union adopted CBAM in 2023—a flurry of activities related to carbon accounting has commenced at the local level. European import regulations, combined with stronger domestic political signals that carbon emissions would become a key benchmark alongside air quality and energy efficiency, have created powerful incentives for both officials and firms to track emissions and calculate product-level carbon footprints. China’s new nationally determined contributions, announced in September 2025 and reiterated at COP30, further elevate carbon reduction as an official target, with potentially significant implications for bureaucratic priorities and cadre promotion.

A survey of ongoing institutional developments and interviews with experts show that municipal and provincial governments are heavily involved in helping firms prepare for the changes in domestic and foreign carbon regulations, most critically CBAM. According to the authors’ calculation, 30 provincial-level carbon accounting platforms have been officially announced (see Table 1). Other provinces have announced general intentions to create similar platforms, but are not included in the current tally. The majority of bureaus remain in the planning (11) or pilot (11) stage, with only seven platforms confirmed to be in operation as of April 2026. All active bureaus were established after 2024, and most in the planning stage are expected to start in 2027. This timing reflects shifts in the regulatory environment, with CBAM being adopted in 2023 (to enter into force in 2026 and expand further by 2028) and China’s own ETS expanding in 2027.

Most of the local bureaus appear to be focused on helping firms conduct product-level carbon accounting, navigate international standards, develop technical specifications, and obtain carbon footprint certifications. Available information on these bureaus’ current and planned activities varies significantly, suggesting that their role is not entirely cemented; many have only just started operating and could shift their focus over time. Still, these bureaus appear to align closely with the 15th Five-Year Plan’s stated goal to “build a national integrated carbon emission data management system, a national greenhouse gas emission factor database, and national carbon measurement laboratories” (authors’ translation).

The authority and funding level of these bureaus also likely vary significantly across regions, which could partially be a result of their bureaucratic placement within the Chinese government system. Some are housed within provincial development and reform commissions, while others sit under ecology and environment bureaus, market administration and supervision agencies, or municipal governments. Central ministries can have downstream effects on bureaucratic behavior at the local level. The National Development and Reform Commission (NDRC), for example, is typically one of China’s more powerful institutions, while the Ministry of Ecology and Environment (MEE) is often characterized as relatively weak. Lack of institutional capacity within the MEE has raised concerns regarding its ability to implement ETS and was identified as a reason for delays in the launch of a national plan. More recently, conflict between the National Energy Agency and the MEE has also been identified as delaying the publication of carbon accounting standards.

Beyond bureaucratic divisions, the finances and internal politics of local governments can also affect ETS and carbon governance implementation. Many of the earliest localities to establish carbon accounting bureaus, such as Guangdong, Zhejiang, Jiangsu, and Shanghai, are among the wealthiest in China and home to many exporting enterprises. For example, Guangdong—and notably Shenzhen—has performed well when it comes to piloting new climate-related initiatives including low-carbon cities, electrification initiatives, and power sector reforms. As another example, the city of Zhenjiang in Jiangsu was a pioneer in introducing carbon management measures well before the rest of the country. Higher income status and corporate interests similarly translate to stronger implementation capacity and political incentives. Although most provinces will likely establish active carbon accounting bureaus by 2030, some will almost certainly prove more effective and influential than others.

It is still too early to assess these bureaus’ long-term impact relative to other factors enabling companies to establish effective compliance with Chinese and foreign regulation. The diverse number of institutions involved in their creation alone suggests that there will be an experimentation and adjustment period. However, their rapid expansion throughout China points to a broader institutional push both to help firms navigate a new regulatory environment and to lay the foundations for a stronger country-wide system of carbon accounting. In other words, even as political incentives around rapid decarbonization remain mixed, China is building the architecture needed for a more robust carbon management and pricing system and CBAM has likely spurred these efforts, at least at the local level.

Intersections with Broader Decarbonization Efforts: A Case Study in Aluminum

China’s aluminum sector is responsible for roughly 60 percent of total global production and provides an illustrative example of how carbon governance has intersected with broader decarbonization efforts. Accounting for about 5 percent of the country’s total carbon emissions, the industry presents a significant obstacle to global emissions reduction. Nonetheless, in China, the CBAM-covered industry has committed to peaking emissions before 2030. Accordingly, since 2017, Chinese firms have relocated as much as 30 percent of domestic aluminum production capacity to regions with abundant clean energy sources. Major companies such as Chinalco have also developed action plans aimed at peaking emissions in response to policies including the 30/60 targets.

Recent policy has reinforced this shift. Since 2020, high-level policies ranging from the so-called 1+N framework to various sectoral implementation and action plans have increasingly emphasized limiting the expansion of manufacturing capacity while increasing efficiency for emission-intensive industries such as aluminum. In 2024, the central government set province-specific targets for renewable energy use in the aluminum industry, ranging from 21 percent for Shandong to 70 percent for Yunnan, where many producers have relocated. Similarly, targets were set in 2025 to boost recycled aluminum production, which requires only about 5 percent of the energy used in conventional processes.

Meanwhile, China has championed “zero-carbon” industrial parks for low-carbon production to supplant an existing ecosystem of as many as 15,000 industrial parks, which has been crucial for the country’s manufacturing and innovation drive. Though a nationwide rollout will take time—the Chinese Government Work Report only mentioned zero-carbon parks for the first time in 2025—their inclusion in the latest five-year plan signals a growing policy emphasis on industrial decarbonization. For tradable commodities such as aluminum, these parks could help lower carbon footprints and improve export competitiveness. Efforts to certify and trade green aluminum have also grown, reflecting domestic and international regulatory pressure as well as a broader interest in tapping into global demand for lower-carbon commodities.

China’s experience with aluminum also underscores the broader challenges facing its decarbonization efforts. Though China’s progress in the sector has likely helped keep global aluminum emissions flat from 2020 through 2022 despite an increase in production, broader progress in emissions reduction has remained uneven across sectors and provinces. On the one hand, China seems to be developing the institutions and some of the incentives needed for a comprehensive carbon emissions reduction strategy. On the other, the government still has not fully used these new tools to push for a rapid transition—in part because slowing growth and rising global tensions have made policymakers wary of economic disruption. These tensions are well recognized within China and are reflected in sector-specific guidance and provincial planning.

Conclusion

China is moving toward instituting a broad system of carbon management and accounting to support its domestic ETS and help firms mitigate the potential negative effects of CBAM. Although these strategies—at least partially inspired by Europe—remain far from fully functional, one conclusion is clear: China is acting decisively to build its energy transition institutional architecture, even as a large implementation gap remains. At present, evidence is mixed as to when—or how forcefully—the central government will push localities and firms toward stricter emissions controls. Nonetheless, China is taking some useful steps toward establishing a sophisticated monitoring, reporting, and evaluation system for carbon, which will likely have positive effects on China’s emission trajectory.

Several questions remain open for future research and will need to be tracked in the coming years. The first relates to China’s ability to convince trading partners, specifically Europe, that its institutions are trustworthy. Without a credible governance system and a broader trust-building effort, Chinese carbon management systems will fail to capitalize on existing complementarities with their European counterparts. Second, the durability of China’s current trajectory to adapt European carbon institutions to local contexts remains uncertain. China’s strategy might shift from one focused on reducing emissions and establishing global climate leadership to one that more squarely prioritizes economic interests and leadership across the clean energy stack. For now, the two goals have been largely complementary, but if international incentives were to disappear, China’s decarbonization efforts could lose momentum.

Developments in Europe will also continue to shape China’s responses. Increasing concerns over energy costs, lagging competitiveness, and geopolitical pressure may affect how CBAM evolves. Measures such as the Industrial Accelerator Act (IAA), which introduces more local content requirements, already suggests a potential shift in the bloc’s strategic orientation. While the draft IAA defers to existing GHG accounting frameworks under the EU ETS for domestic products and CBAM for imports, concerns that these systems impose excessive burdens on European businesses have encouraged efforts to relax requirements for smaller firms. If CBAM becomes more protectionist than decarbonization-oriented, incentives for countries including China would change accordingly. The Chinese government is following these developments closely and has already criticized the IAA as protectionist, echoing its broader critique of CBAM.

For now, China’s institutional evolution for carbon governance suggests that far more attention needs to be paid to how trade defense mechanisms such as CBAM can influence other countries’ behavior. In China’s case, CBAM appears to have accelerated parts of an existing carbon governance agenda and may function as a forcing mechanism to ensure compliance. This will be especially important for U.S. stakeholders, who may be considering potential carbon tariff policies to meet multiple objectives including economic competition with China. Indeed, China’s policy evolution in recent years suggests that it may be able to narrow its carbon gap with the United States through coordinated and sustained interventions, especially if the latter fails to make the investments and policy commitments needed to preserve its carbon-intensity advantage.

Finally, the developments tracked in this paper show that China’s adoption of European-style institutions is progressing. Although many hurdles remain before China’s ETS can even be considered eligible for linking with the EU ETS, the general convergence should be evaluated by U.S. policymakers as a sign of where governance of trade and carbon might be headed in the coming years. Despite recent U.S. retrenchment, climate-oriented institutions are poised to continue to shape how China and the European Union—two of the world’s largest trading partners—engage with each other and influence rest of the world in the process. When the United States chooses to reengage with global emissions governance, it may find that the rules have been rewritten in its absence.

Ilaria Mazzocco is deputy director and senior fellow with the Trustee Chair in Chinese Business and Economics at the Center for Strategic and International Studies (CSIS) in Washington, D.C. Ray Cai is an associate fellow in the Energy Security and Climate Change Program at CSIS.

The authors would like to thank Ryan Featherston for his key help in this project; Weila Gong, Scott Moore, and Yan Qin, for feedback on earlier versions of the draft; research interns Andy Yang, Qingfeng Yu, Caroline Kiely, Aaron Yang, Eleanor Randolph, and Antonio Tintoré Vincent. All mistakes are solely the authors’.