Demand

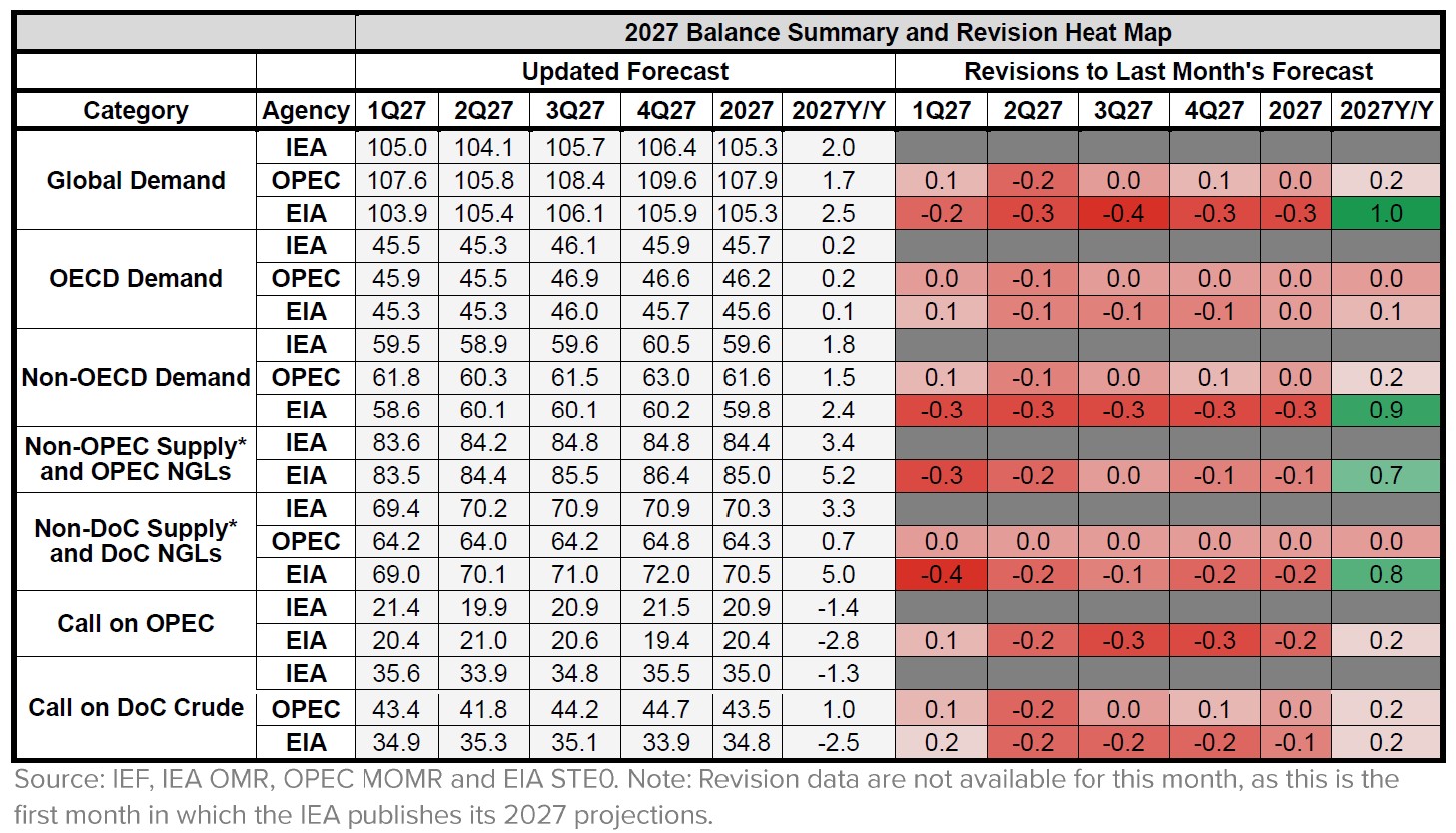

OPEC: OPEC revises its 2026 global oil demand growth forecast downward by 0.2 mb/d relative to the previous month’s assessment, to 1.0 mb/d year-on-year. Demand growth continues to be driven by non-OECD economies (0.9 mb/d), while OECD demand expands modestly (0.1 mb/d). For 2027, OPEC raises its growth projection by 0.2 mb/d to 1.7 mb/d, supported by demand growth of 1.5 mb/d in non-OECD countries and 0.2 mb/d in OECD economies, increasing global demand to 107.9 mb/d.

EIA: EIA revises its 2026 global oil demand outlook to a contraction of 1.1 mb/d, representing a 1.3 mb/d downward revision relative to the previous month’s assessment and a 2.3 mb/d reduction compared with its February outlook. The weaker outlook reflects poli cy measures aimed at curbing oil consumption, fuel supply shortages, and declining exports of refined petroleum products. In contrast, EIA expects oil demand to rebound in 2027, with growth reaching 2.5 mb/d, raising global oil demand to 105.3 mb/d.

IEA: IEA lowers its 2026 global oil demand growth forecast to a contraction of ~1.1 mb/d year-on-year, approximately 0.7 mb/d below the previous month’s projection. For 2027, the agency projects a strong rebound, with demand increasing by ~2.0 mb/d, supported by a recovery in global trade, lower oil prices, and stronger economic growth, bringing global demand to 105.3 mb/d.

Supply

OPEC: OPEC leaves unchanged its outlook for non-DoC liquids supply and DoC NGLs growth at ~0.8 mb/d in 2026, placing total supply to ~63.6 mb/d. Supply growth is led by the United States, Canada, Brazil, and Argentina. The 2027 projection also remains unchanged, with supply expanding by 0.7 mb/d year-on-year to ~64.3 mb/d, supported primarily by Canada, Qatar, Brazil, and Argentina.

EIA: EIA revises downward its outlook for non-DoC liquids supply and DoC NGLs, projecting a contraction of ~1.6 mb/d year-on-year in 2026, 0.7 mb/d below the previous month’s assessment. The outlook rebounds in 2027, with supply growth increasing to 5.0 mb/d, 0.8 mb/d above last month’s projection. The EIA raises its forecast for US crude oil production to ~13.7 mb/d in 2026 and ~14.2 mb/d in 2027, both approximately 0.1 mb/d higher than in the previous month’s outlook.

IEA: IEA projects global liquids supply to average 102.4 mb/d in 2026, down 3.9 mb/d year-on-year, before rising to 110.3 mb/d in 2027, an increase of 8.0 mb/d. IEA estimates of non-DoC supply and DoC NGLs growth to increase by 0.2 mb/d y/y to 67.0 mb/d in 2026. The IEA revised down its non-OPEC supply and OPEC NGLs downward by 0.3 mb/d y/y, bringing average full year value to 81.0 mb/d.

2025-2027 Balance Summary

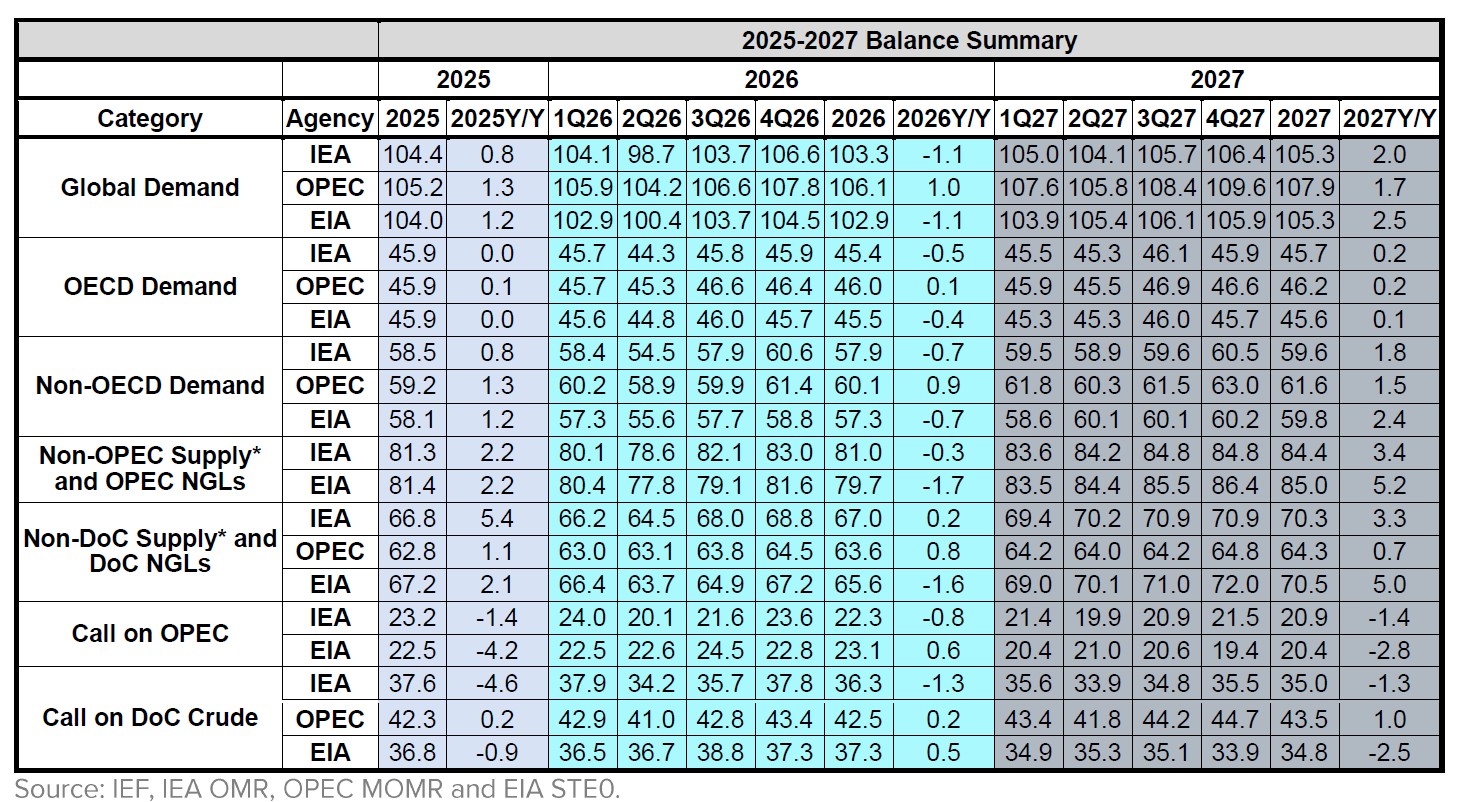

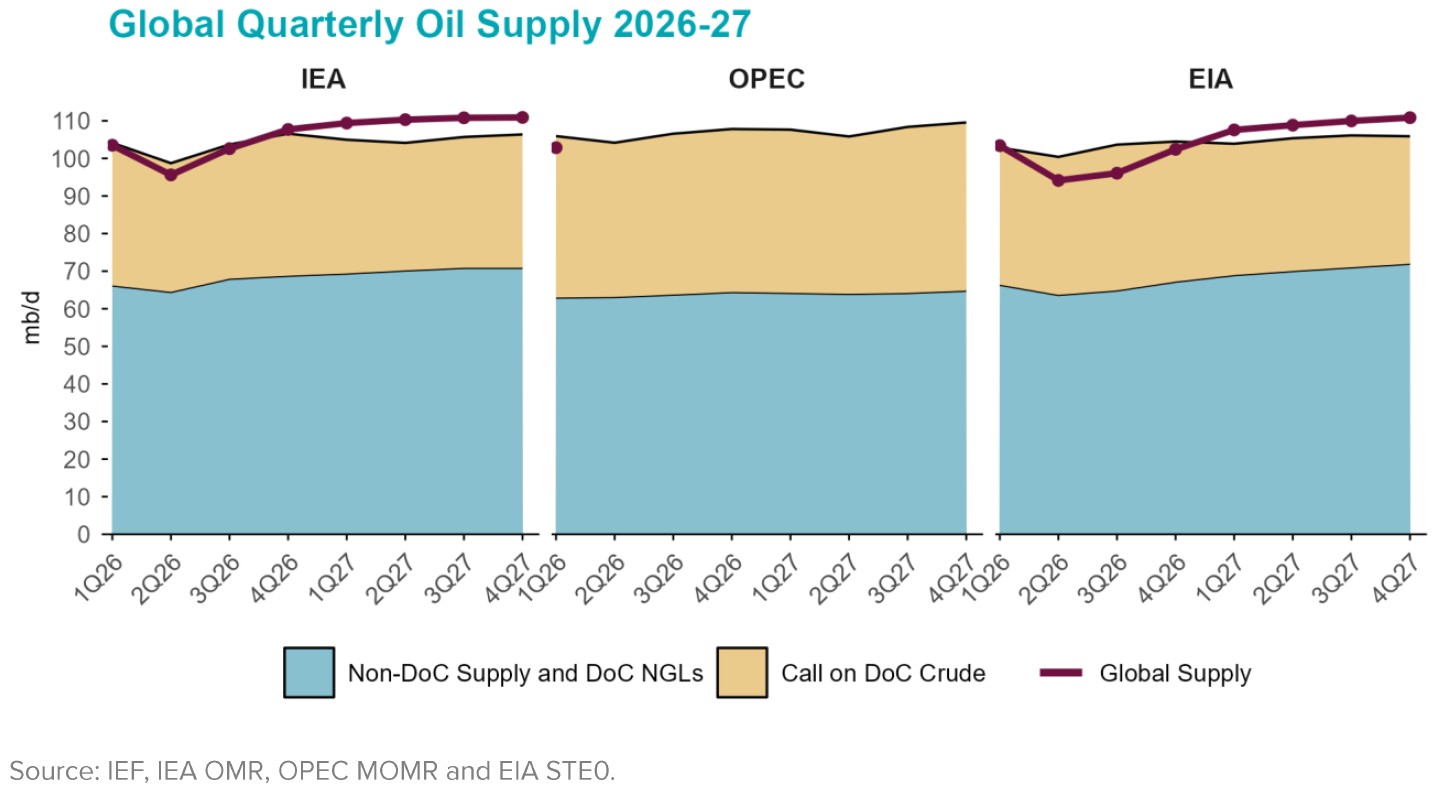

Global demand projections diverge notably across agencies in 2026, with the differences narrowing in 2027. In volume term, the EIA and IEA estimate global demand at 102.9 and 103.3 mb/d, respectively, in 2026, while OPEC projects substantially higher at 106.1 mb/d, representing a 2.8 –3.2 mb/d spread. This pattern persists into 2027, where EIA and IEA converge at 105.3 mb/d against OPEC’s 107.9 mb/d estimate, a 2.6 mb/d differential.

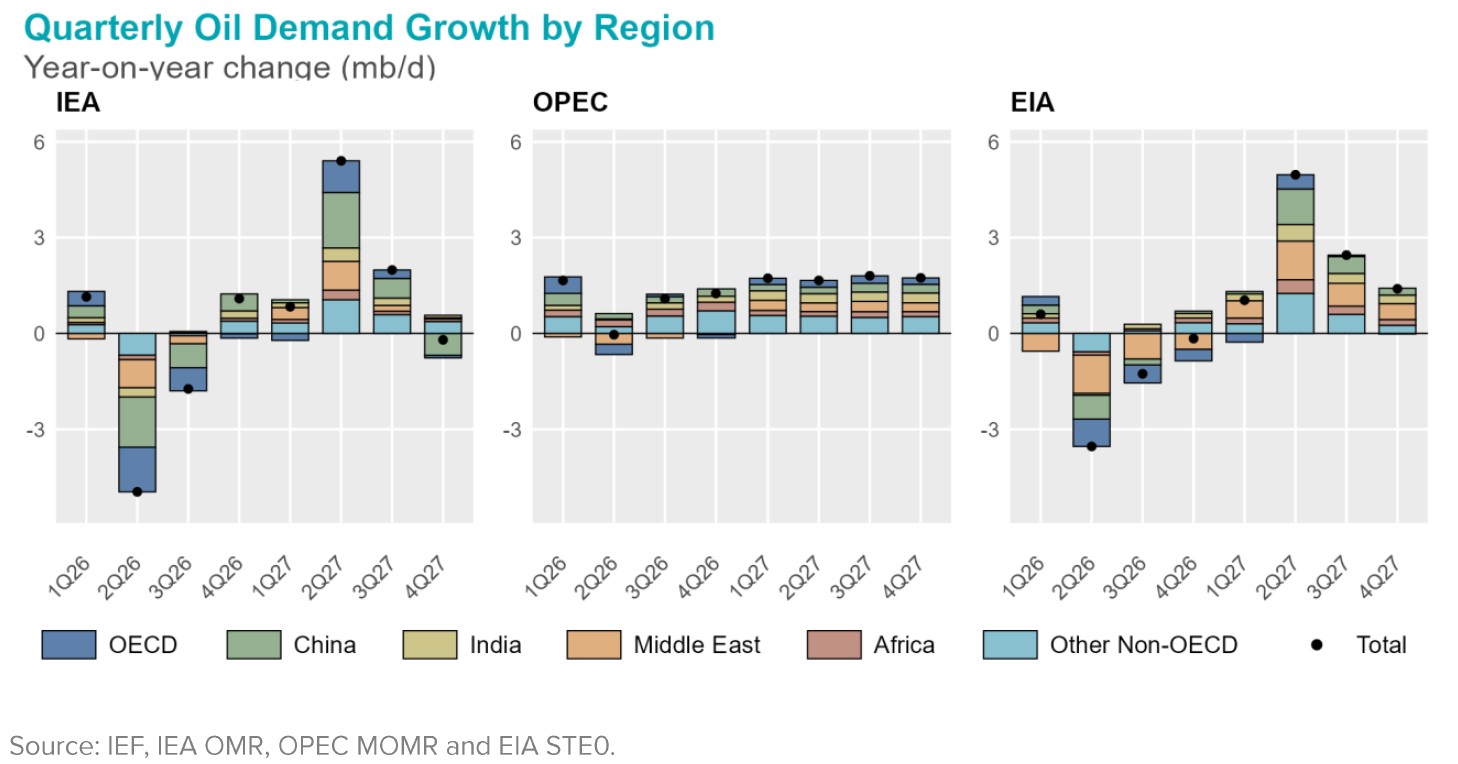

OPEC projects the strongest oil demand growth in 2026, with first-quarter growth reaching 1.6 mb/d, while the EIA reports the weakest outlook at 0.6 mb/d, resulting in a spread of around 1.0 mb/d. In the second quarter, OPEC’s demand growth remains close to zero, whereas the IEA projects a decline of around 5.0 mb/d, representing the largest downward adjustment across all quarters. Looking ahead to 2027, both the IEA and EIA project a recovery in global oil demand, supported by stronger demand growth in China, the Middle East, and other emerging economies.

In 2026, the EIA and IEA project broadly similar levels of non-DoC liquids supply and DoC NGLs, with quarterly differences generally below 1.0 mb/d, except in 3Q26 where the gap widens to 3.1 mb/d. By contrast, OPEC consistently projects lower non-DoC supply, remaining 1.2–4.5 mb/d below the EIA and IEA. The alignment between the EIA and IEA strengthens further in 2027, with quarterly differences narrowing to 0.1–0.4 mb/d, while OPEC’s projections remain 5.2–7.2 mb/d lower throughout the year.

2026 Outlook Comparison

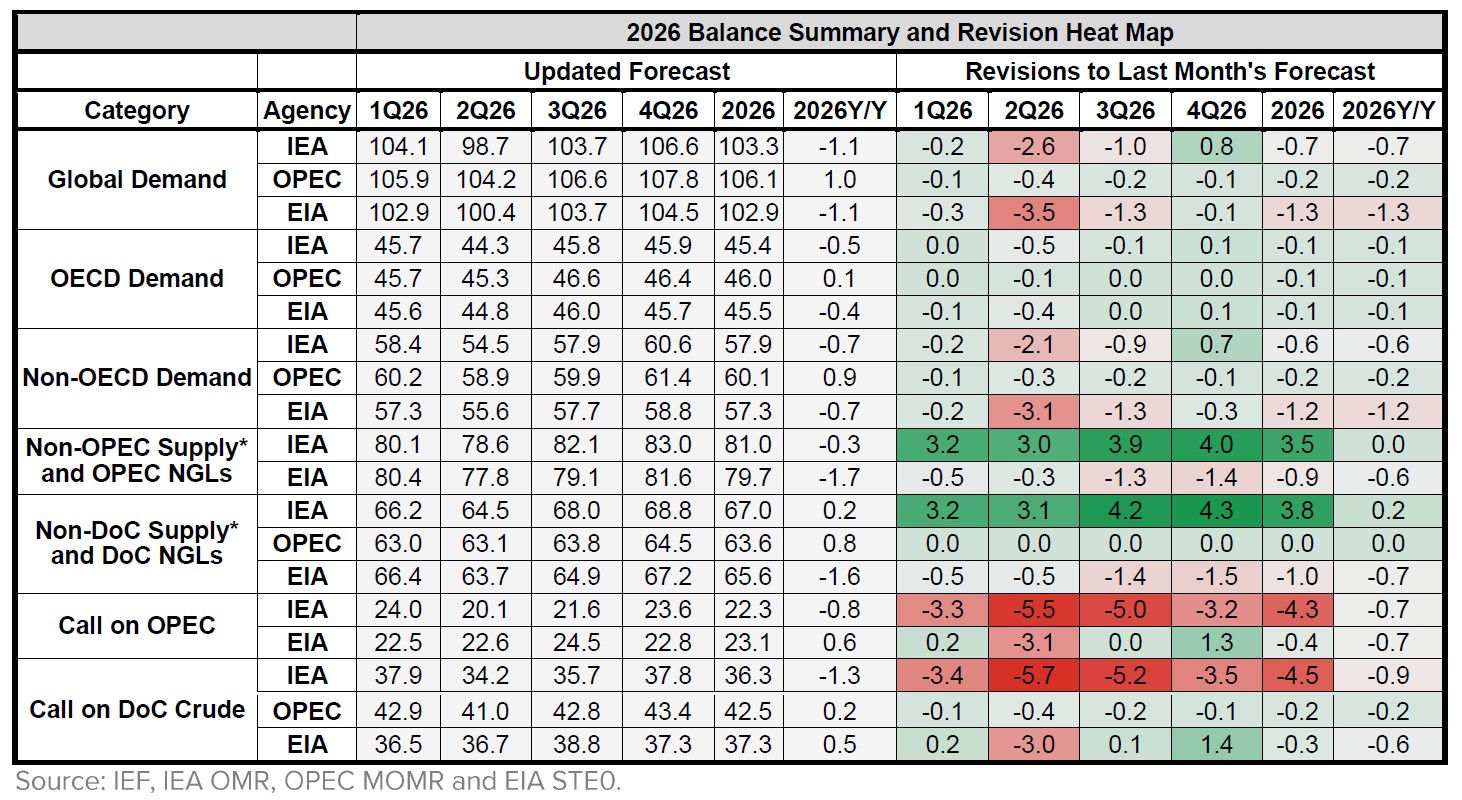

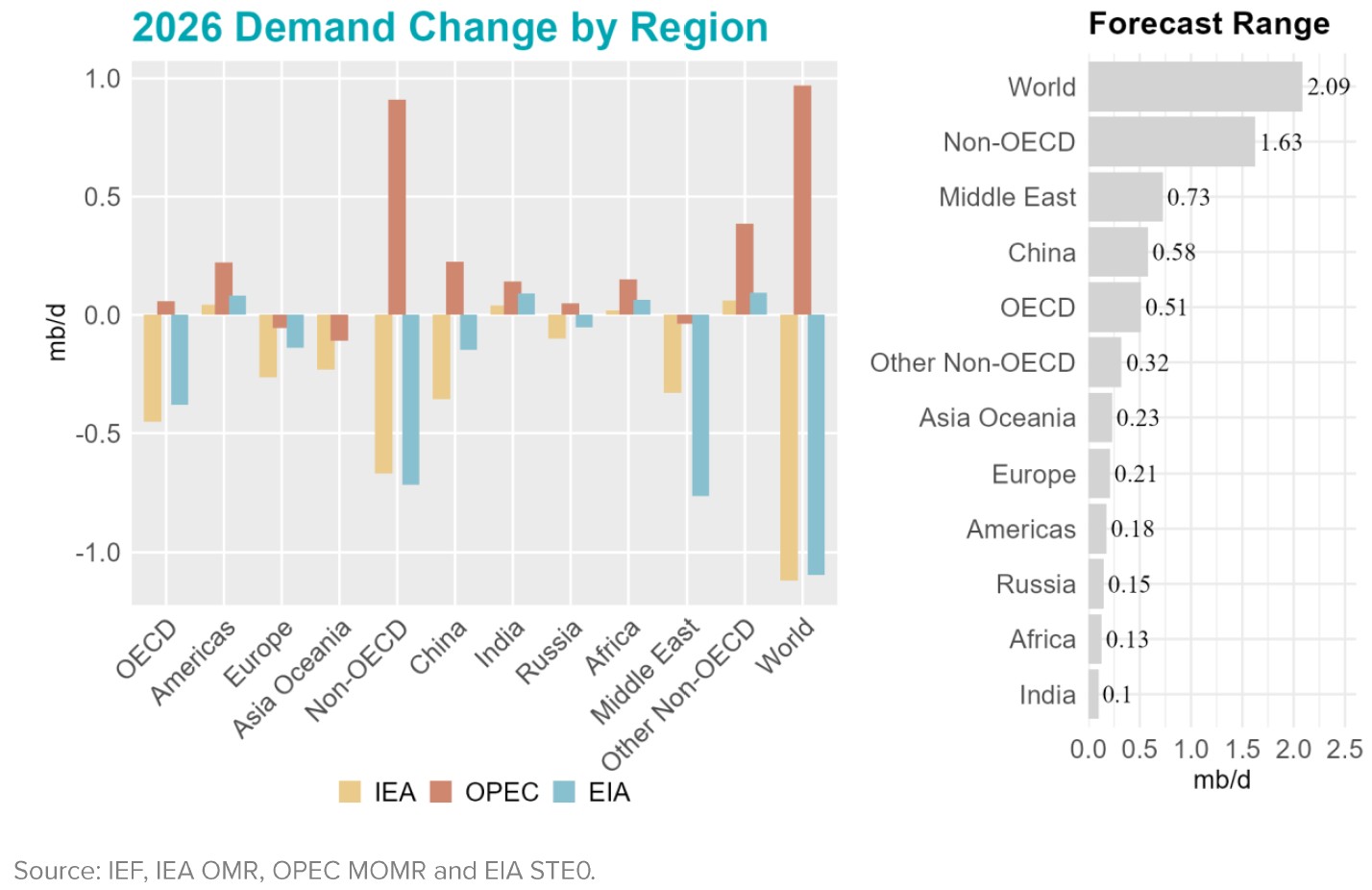

Global oil demand projections for 2026 remain highly divergent across agencies, ranging from a contraction of 1.1 mb/d in both the EIA and IEA outlooks to growth of 1.0 mb/d in OPEC’s assessment, a spread of 2.1 mb/d. The divergence persists across both OECD and non-OECD economies. Compared with the previous month’s outlook, all three agencies revise their 2026 demand projections downward by 0.2–1.3 mb/d year-on-year.

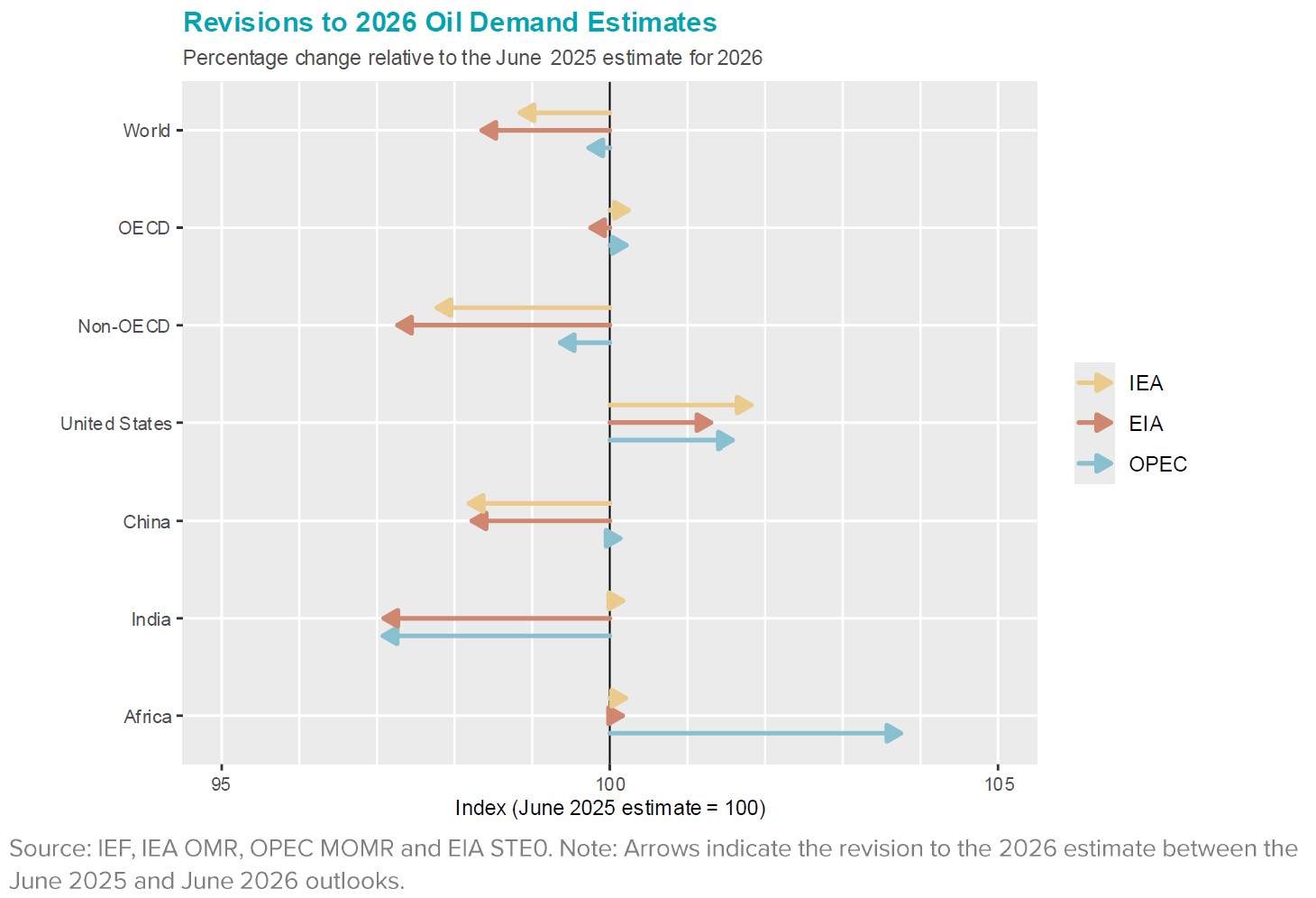

Recent revisions to 2026 oil demand estimates are driven primarily by adjustments in non-OECD economies, where the EIA (−2.7%) and IEA (−2.2%) make substantially larger downward adjustments than OPEC (−0.6%), while OECD revisions remain limited across all three agencies. More notable differences emerge at the regional level. The United States is revised upward across all three outlooks, with the largest increase in the IEA assessment (+1.8%). Africa also records upward revisions across all agencies, led by OPEC (+3.8%), whereas the IEA and EIA make only marginal adjustments. By contrast, China is revised downward by the IEA and EIA but remains broadly unchanged in the OPEC outlook, while India shows the greatest divergence, with the IEA maintaining a near-baseline projection and both OPEC and the EIA lowering demand by around 3%.

Evolution of 2026 Annual Demand Growth Forecasts

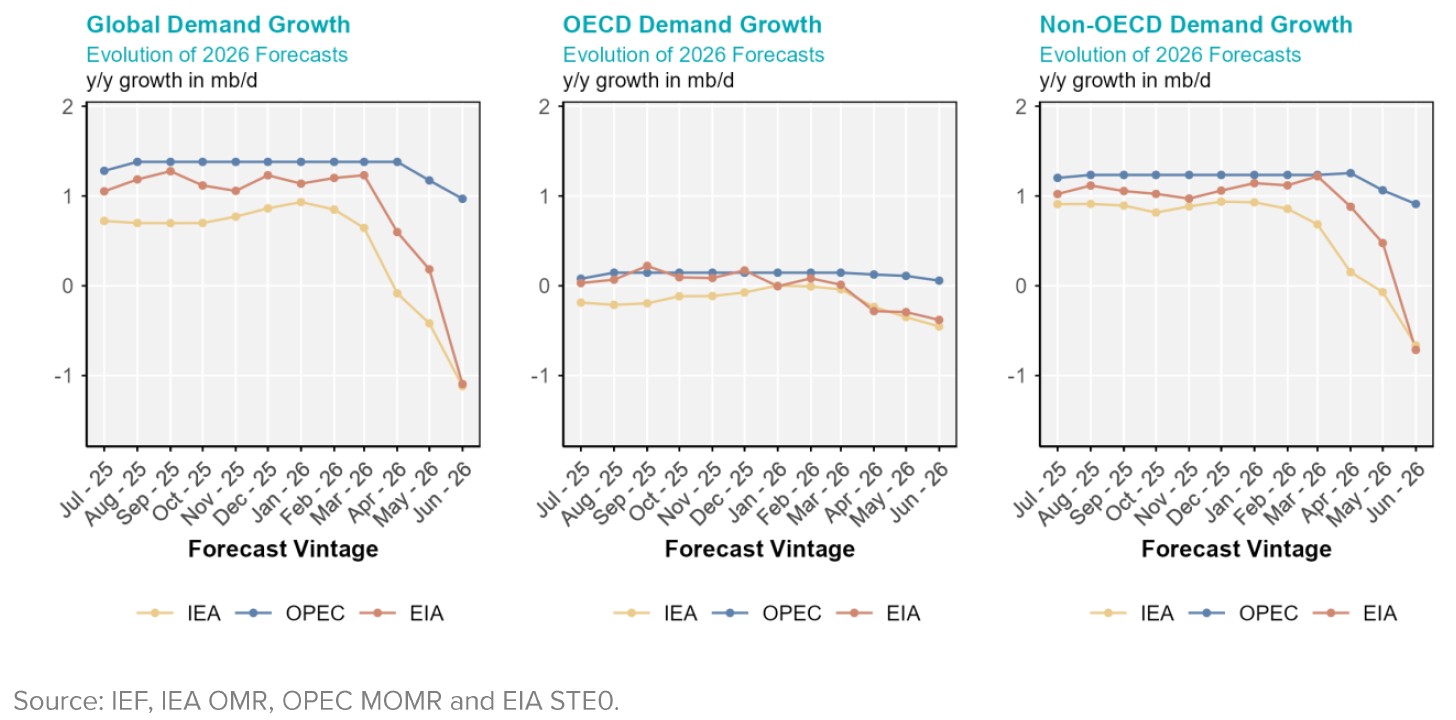

The three agencies diverge substantially on global demand growth. In January 2026, OPEC projects 1.4 mb/d growth, while IEA and EIA estimate 0.9 and 1.1 mb/d respectively, establishing a 0.5 mb/d spread. This gap widens significantly by June, where IEA and EIA both forecast negative growth at −1.1 mb/d, whereas OPEC maintains growth at 1.0 mb/d, creating a 2.1 mb/d spread.

OECD demand contracts consistently in both the IEA and EIA outlooks, while OPEC projects broadly flat demand. Non-OECD economies show a similar downward trend in the IEA and EIA assessments, with demand declining by around 0.7 mb/d in both cases, whereas OPEC continues to project growth of 0.9 mb/d. Within the non-OECD region, both the IEA and EIA forecast declining demand in China, while India and Africa record modest demand growth across all three agencies.

2027 Outlook Comparison

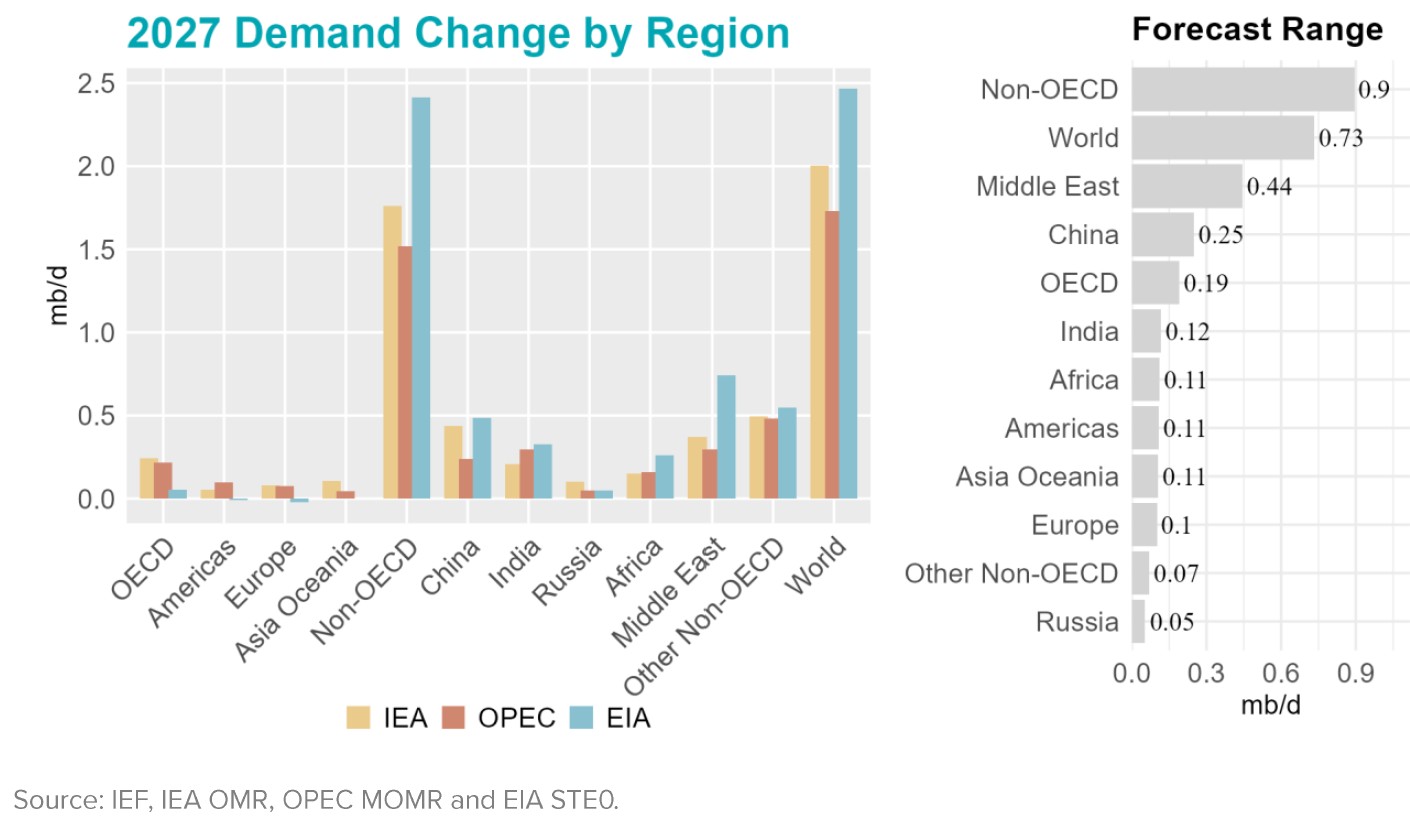

Following the downward revisions to 2026, all three agencies project a recovery in global oil demand in 2027. The EIA forecasts the strongest growth at 2.5 mb/d, followed by the IEA (2.0 mb/d) and OPEC (1.7 mb/d). The expansion is driven primarily by non-OECD economies, while OECD demand also returns to growth. On the supply side, the EIA projects the strongest increase in non-DoC liquids supply and DoC NGLs ~5.0 mb/d year-on-year, compared with 3.3 mb/d in the IEA outlook and ~0.7 mb/d in OPEC’s assessment.

At the regional level, non-OECD economies account for 95–99% of projected global demand growth across all three outlooks. China continues to account for a substantial share of global demand growth, adding 0.2–0.5 mb/d, while India adds 0.2–0.3 mb/d and Africa contribute 0.15–0.26 mb/d. Across regions, the EIA generally projects stronger demand growth than both the IEA and OPEC.